IVF Insurance Coverage: Your Quick Guide to Getting Help Pay for Fertility Treatment

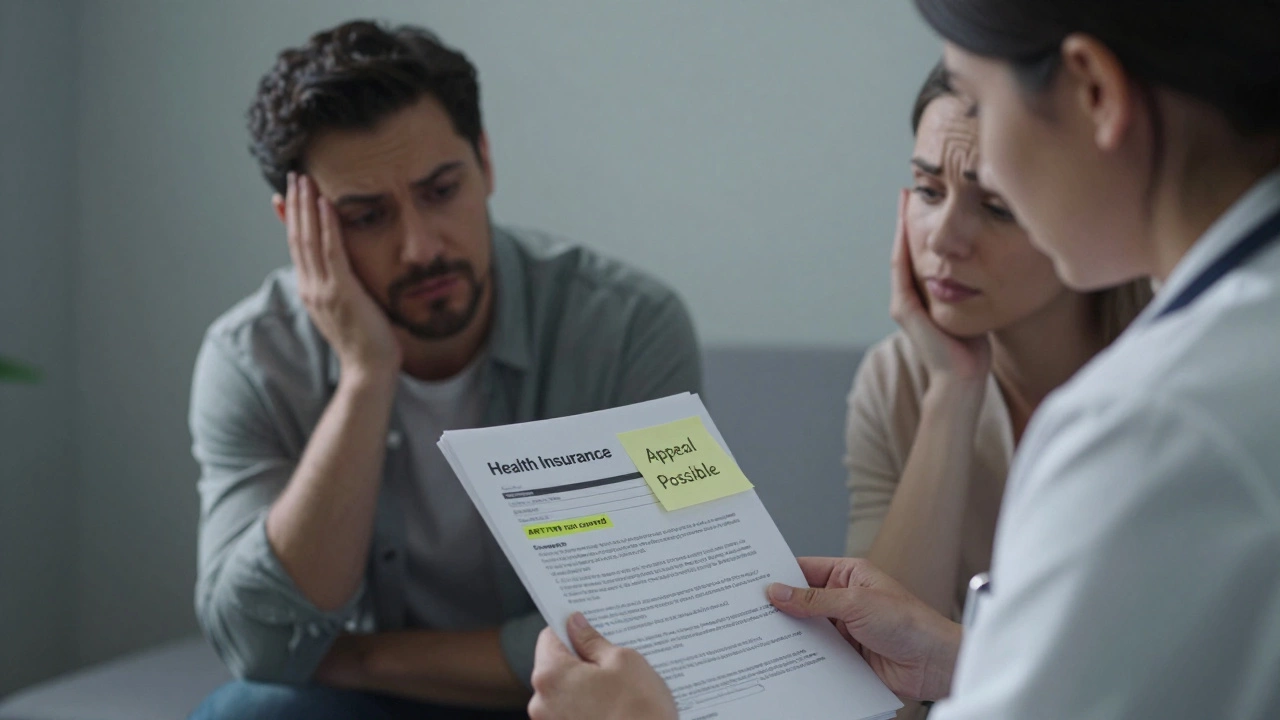

If you’re thinking about IVF, the first thing most couples wonder is – will my insurance help? The short answer is: some plans do, many don’t, and the rules keep changing. Knowing where to look, what to ask, and how to file a claim can save you a lot of stress and money.

What Types of Policies Touch IVF in India?

In India, government‑run schemes such as Ayushman Bharat usually focus on life‑saving procedures, not fertility. Private insurers, however, have started adding IVF riders or specific fertility add‑ons to high‑end health plans. Look for terms like “fertility coverage,” “IVF rider,” or “assisted reproductive technology (ART) benefit” in the policy document.

Most of these riders cover a percentage of the total IVF cost – often 50‑70 % – up to a ceiling that ranges from ₹50,000 to ₹2 lakh per cycle. Some premium‑priced plans even include medication costs, which can be a big portion of the bill.

How to Check If Your Current Plan Has IVF Benefits

First, pull up the summary of benefits on your insurer’s website or app. If you don’t see anything about fertility, call the customer service line and ask directly: “Do you offer any coverage for IVF or other assisted reproductive technologies?” Write down the reference number and the name of the rep for future follow‑up.

When you talk to an agent, ask these five questions:

- Is IVF listed under the “procedural cover” or as a separate rider?

- What is the maximum amount the insurer will pay per cycle?

- Are the medications (like gonadotropins) covered, and if so, up to what limit?

- Do you require a pre‑authorization from a specific network clinic?

- What paperwork is needed (doctor’s prescription, treatment plan, cost estimate) before filing?

Getting clear answers early stops the surprise of a denied claim later.

Tips to Boost Your IVF Coverage

1. Buy a rider before you start treatment. Most insurers only apply the rider retroactively if you add it at least 30 days before the first IVF appointment.

2. Bundle with a comprehensive health plan. Some higher‑tier policies automatically include a modest IVF benefit without an extra rider – it’s worth checking if you’re renewing soon.

3. Use a network clinic. Insurers often give higher reimbursement rates if you go to a hospital or clinic that’s part of their network.

4. Document everything. Keep copies of doctor’s letters, lab reports, medication receipts, and the cost estimate. Submit claims within the insurer’s timeline – usually 30 days from the date of service.

5. Consider a supplemental policy. If your main plan offers little, a low‑cost standalone fertility rider can still cover a portion of the cycle and meds.

Common Pitfalls to Avoid

Don’t assume “fertility” means “IVF.” Some policies only cover diagnostic tests or medication, leaving the actual embryo transfer out of scope. Also, watch out for caps that reset every year – you might need to plan multiple cycles within a single policy year to get the most out of the limit.

Another mistake is ignoring the pre‑authorization step. A denied pre‑approval means you’ll have to pay full price and then try to claim, which most insurers reject.

Bottom Line

IVF insurance in India isn’t universal, but it’s getting better. The key is to read the fine print, ask the right questions, and act early – especially if you need a rider. By matching a suitable plan with a network clinic and keeping detailed records, you can cut down the out‑of‑pocket cost and focus on what matters most: building your family.

Will Insurance Cover IVF? What You Need to Know in 2026

Will your health insurance cover IVF in India? Find out what's covered, what's not, and how to get financial help for fertility treatment in 2026.

Understanding Which Insurance Plans Cover IVF

Navigating insurance coverage for IVF can be confusing, but understanding the basics can help. This article explores how different insurance plans handle IVF coverage and provides practical tips for those seeking fertility treatments. We'll dive into state mandates, common policy terms, and steps to improve coverage chances. Taking charge of the process can ease financial worries and focus on what's important – building a family.

What Organ Is Metformin Hard On? Know the Real Risks

Apr, 24 2025

What You Shouldn't Tell Your Therapist

Feb, 25 2025